A practical, first-principles approach to evaluating venture liquidity strategies and portfolio management.

Venture capital is in a liquidity gridlock. While the IPO market has begun to reopen and distributions have resumed, there is a significant backlog that can not—and we believe will not—be met via IPOs and M&As alone. Venture firms have built exceptional private value; there are roughly 63,000 U.S. venture-backed companies1 and over $4 trillion in global venture capital assets under management.2 Realizing that value at the right time, price, and structure is increasingly complex.

As GPs face growing pressure to deliver DPI, secondaries have become a core tool for portfolio management, with annual volume of direct secondaries projected to exceed $80 billion as of Q3 2025.1 Despite rising activity, venture secondaries remain a developing market. Most deals are bespoke, pricing can be opaque, and processes often vary by counterparty. That makes clarity of purpose even more important.

To identify the right secondary approach, GPs must start from first principles: what are they solving for? Is the goal to return a set dollar amount of DPI? To recycle capital within a specific fund? To manage orphaned assets after team changes? Or to take money off the table in high-performing companies? The priority can help dictate the best path.

At NewView Capital, we believe liquidity should be managed with the same discipline that drives great investing, with a focus on intrinsic value and long-term alignment across investors and companies. We developed this guide to help fellow GPs navigate secondaries with clarity, discipline, and conviction. While there is no one-size-fits-all playbook, understanding the leading options, and their benefits and trade offs, is the first step to choosing the right path for your firm.

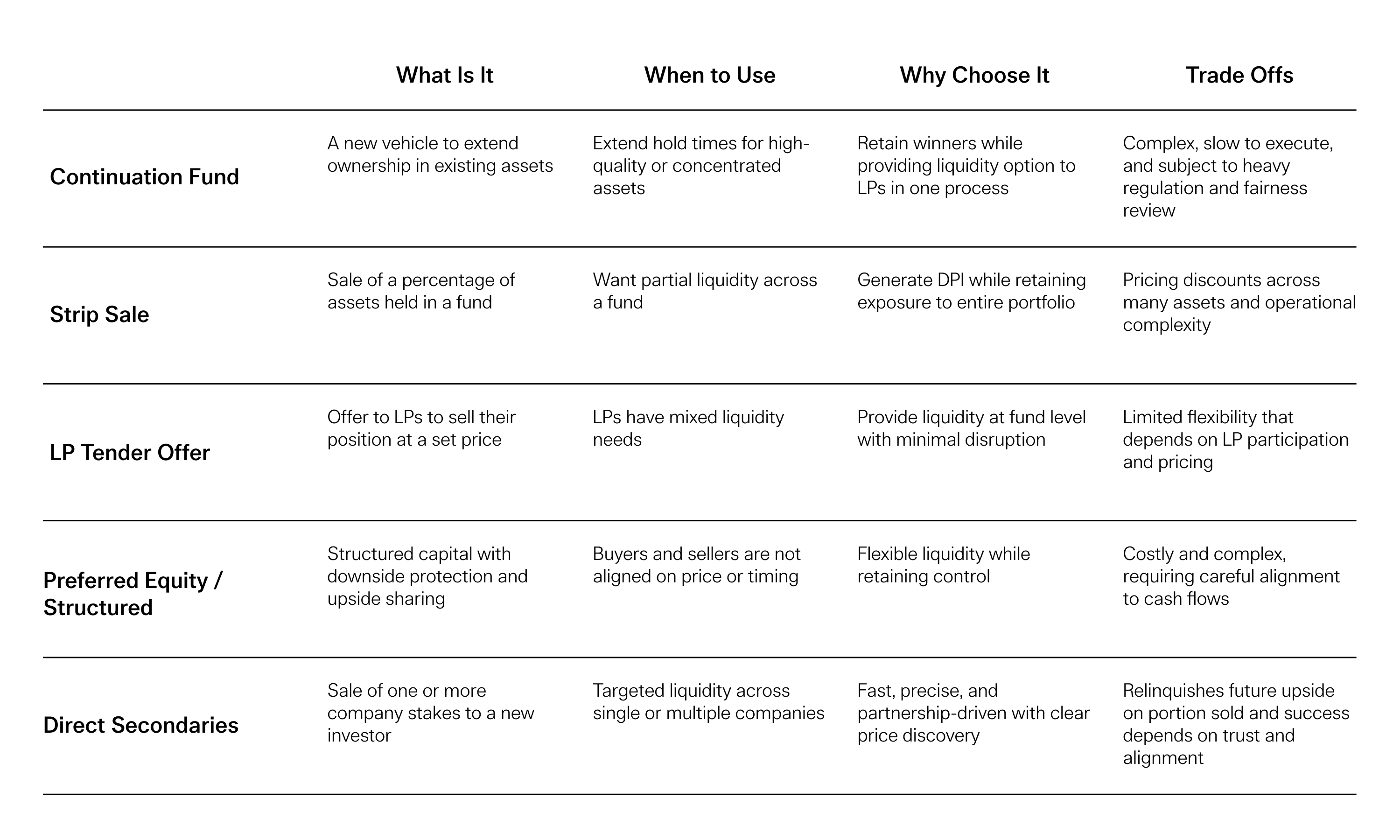

Continuation Funds

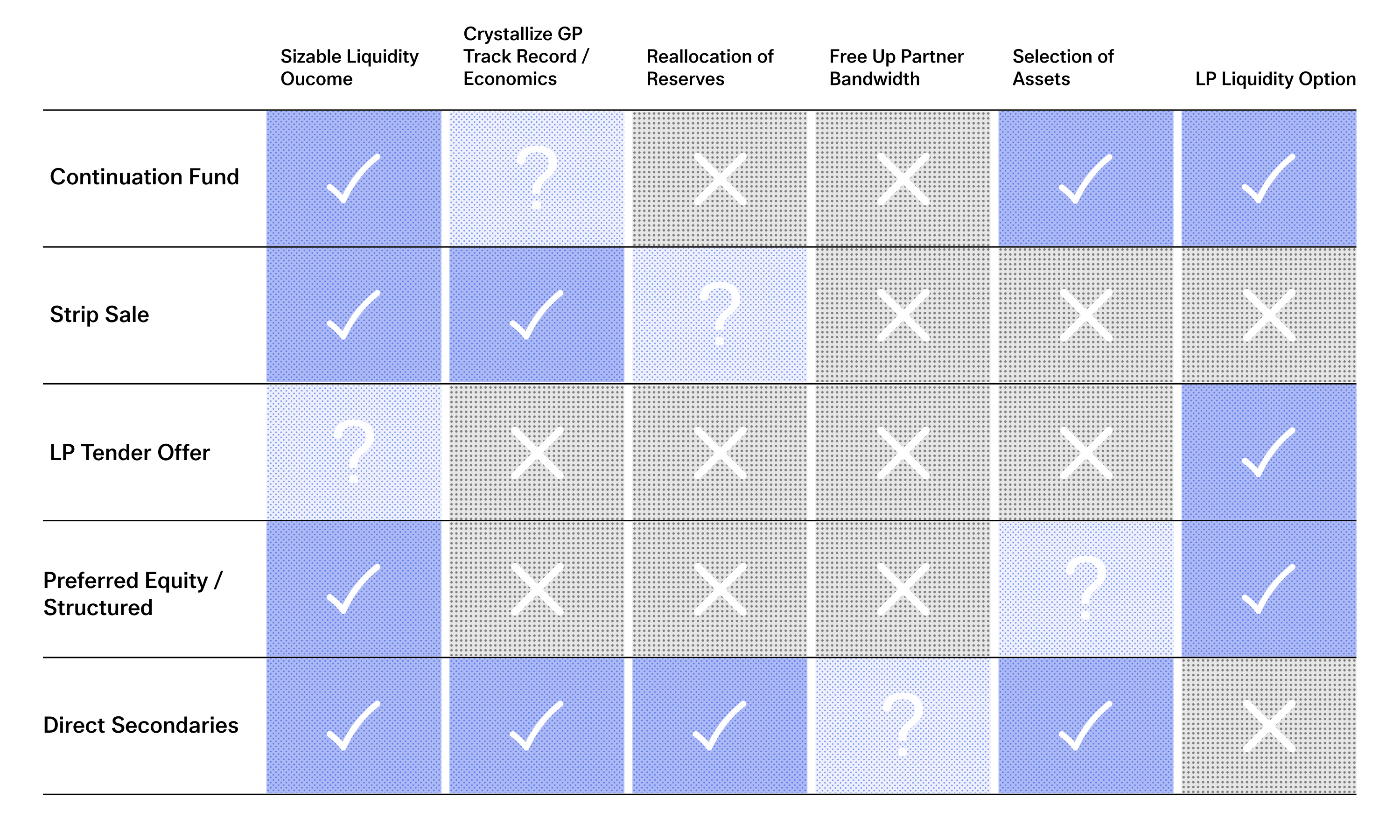

Extends ownership in winners while providing LPs liquidity but are slow and complex to execute

Continuation funds allow GPs to move one or more portfolio companies into a new vehicle, offering existing LPs the choice to roll forward or sell.

Over the past year, the initial enthusiasm for continuation funds has been tempered by the realities of execution. Venture lacks the scale, valuation transparency and advisory infrastructure of private equity, making these transactions more difficult to close due to limited buyer depth, smaller deal sizes, and a higher bar for required returns. CVs work best for sought after, high-conviction assets that have a track record of growth that is expected to continue.

Continuation vehicles are among the most complex and time consuming to execute. They require coordination across LPs, portfolio companies, advisors, and new investors. Fair pricing requires third-party validation through valuations, LPAC approvals, and competitive bids from secondary buyers in a shallow venture market. These transactions often take several quarters and rely on clear communication and alignment to maintain confidence among stakeholders.

Non-RIA managers face additional structural hurdles. Firms relying on the venture capital adviser exemption are not permitted to hold more than 20% in non-qualifying assets at the fund level, which can make a traditional continuation fund infeasible. A ‘synthetic’ approach is possible but requires splitting the existing partnership into sub partnerships, amending the LPA, and obtaining LP consent, a costly and time-consuming process that carries regulatory risk if later deemed non-compliant.

For the right manager, CVs can elegantly extend ownership, deliver liquidity to LPs, and demonstrate conviction, but they demand significant preparation and alignment. These transactions are typically backed by large secondary funds and institutional LPs that can underwrite multi-asset portfolios within venture and growth equity.

Practical considerations:

Will regulatory or fund constraints (e.g. the 80 percent test) affect feasibility?

Are LPs aligned on the rationale and overall structure?

Is the GP team eligible for a carry reset or other incremental economics?

Is the portfolio composition compelling and supported by clear selection criteria?

Has an independent fairness opinion and valuation been completed to validate pricing?

Example:

A large multi-stage manager pursued a continuation vehicle to extend ownership across a curated portfolio of ten late-stage companies with strong growth potential. The initial proposal drew pushback from LPs who felt the mix included too many mid-performing assets and not enough of the manager’s top-tier holdings. In response, the GP re-curated the portfolio to include a greater concentration of high-quality companies, engaged an independent valuation advisor, and invited multiple secondary buyers to provide competitive bids. To maintain alignment, the firm shared detailed company-level data, held several LPAC sessions to review structure and economics, and clarified how carried interest would be allocated between vehicles. The revised transaction gained broad support, delivering liquidity to selling LPs while allowing the GP to retain and continue supporting its most valuable assets. The process took roughly nine months from initiation to close.

Strip Sales

Creates partial liquidity across a portfolio while preserving fund control

Strip sales allow GPs to sell a partial, non-controlling interest across a portfolio, typically 20 to 30 percent of each company, to a secondary buyer. These transactions provide liquidity without changing fund terms and can unlock value mid-fund without disrupting governance.

They are especially useful for GPs managing broad portfolios where multiple companies still have meaningful upside. Strip sales can return capital to LPs, reinforce DPI ahead of a fundraise, relieve pressure on follow-on reserves, and preserve control. These transactions generally attract secondary funds and institutional LPs seeking diversified venture exposure.

Because they involve many assets, strip sales are often complex. Negotiating across a full portfolio requires close coordination between the GP, secondary buyer, and portfolio companies to align on scope, valuation, and transfer mechanics. Pricing can also be more challenging as buyers don’t have discretion and must underwrite a cross-section of assets. This can result in higher discounts than for direct multi-asset or single-asset sales.

Practical considerations:

How will the portfolio be priced? Asset by asset or on a blended basis?

Will LPs support the rationale and treatment of proceeds?

How will buyer diligence across multiple companies affect the timeline and execution?

Does the structure retain sufficient exposure to high-conviction assets?

Will pricing dynamics impact the holding value of remaining ownership?

Example:

A GP managing a 2015 fund with 30 active companies and a new fundraise approaching needed to demonstrate DPI without giving up control of its best assets. The firm pursued a 25 percent strip sale across the portfolio, providing partial liquidity to LPs and freeing up reserves for follow-on investments. To coordinate the sale, the GP needed to obtain transfer consent from each company and update valuations to reflect uneven performance across sectors. The GP organized and managed the process directly, preparing data room materials, aligning company management teams on disclosure, and engaging with multiple buyers to benchmark pricing. Negotiations focused on achieving fair blended valuation while preserving future upside participation. The transaction returned capital to LPs and preserved governance rights while giving the buyer diversified exposure across the fund’s entire portfolio.

LP Tender Offers

Offers optional liquidity to LPs without altering fund structure

LP tender offers allow GPs to offer liquidity to existing LPs at a negotiated price usually facilitated by a secondary buyer. LPs can choose whether to participate, while the fund’s structure and underlying assets remain unchanged.

This structure is most useful when some LPs are seeking liquidity and others prefer to hold. It allows the GP to meet divergent investor needs without restructuring the fund or selling specific assets. It can also be a useful way to clean up the LP base or offer flexibility without altering fund construction.

While operationally straightforward, LP tenders offer less control than other secondary structures. The GP cannot select which LPs will participate as sellers and limited uptake may reduce the usefulness of the process. Pricing is typically driven by market appetite rather than intrinsic asset value and timing depends on LP responsiveness. These transactions are typically led by secondary funds, sometimes alongside institutional LPs or fund-of-funds, acquiring LP interests through GP-organized processes.

Practical considerations:

How will pricing be determined and communicated to LPs?

Will participation levels be sufficient to complete the transaction?

Are selling LPs’ motivations aligned with the fund’s long-term strategy?

Has the LPAC reviewed and approved the process?

Example:

A GP managing a 2018 fund heard from several LPs, mostly smaller family offices, that they were over-allocated and wanted liquidity. The larger institutional LPs preferred to hold. The GP needed a way to meet these divergent needs without restructuring the fund, so they arranged a tender offer for up to 20 percent of the fund backed by a single secondary buyer. The process required coordination across LPs with varying liquidity goals as well as clear communication to maintain alignment and trust. The GP worked with counsel to prepare detailed disclosures and positioned the transaction as part of proactive portfolio management ensuring participation was entirely optional and pricing reflected fair market value. The offer was fully subscribed, providing liquidity to selling LPs while preserving continuity for long-term investors and reinforcing confidence ahead of the next fundraise.

Preferred Equity and Structured Solutions

Delivers flexible capital for liquidity without selling ownership

Structured solutions such as preferred equity, profit sharing notes, and other hybrid instruments allow GPs to raise capital against a fund or asset without triggering a sale. These structures are typically used to provide interim liquidity, refinance obligations, or fund follow-ons when exits are slow or valuations are misaligned.

Preferred equity sits between debt and equity. Investors receive downside protection and a return with optional upside sharing tied to future cash flows, typically attracting secondary and credit-oriented investors offering flexible liquidity solutions. These deals can be negotiated at the fund or asset level and are especially useful when buyers and sellers aren’t aligned on valuation or timing.

For GPs with conviction in future value, structured solutions can create liquidity without giving up control, exposure, or board seats. They offer flexibility in tailoring terms to portfolio performance, reserve strategy, or LP dynamics.

While powerful, these deals are complex, often expensive, and LP sentiment about these structures is mixed to negative. Structuring repayment waterfalls takes time and legal support, and the cost of capital may be high relative to selling assets. Poorly designed structures can create misalignment, cash flow stress, or excessive dilution if exits take longer than expected. They are best suited for managers with predictable near-term liquidity events and a clear rationale for raising capital without selling.

Practical considerations:

What visibility is needed to underwrite repayment terms?

Will repayment be tied to specific exits or overall fund cash flows?

How will preferred returns flow through to existing LP distributions?

Are governance and incentives aligned between GP and capital provider?

Example:

A GP managing a 2016 fund with several late-stage winners and upcoming financings needed liquidity to support follow-ons while maintaining exposure to key assets. With limited reserves and few near-term exits, the GP structured a preferred equity solution at the fund level to unlock capital without changing ownership. The structure provided upfront liquidity in exchange for a capped share of future proceeds, allowing the GP to fund follow-ons and deliver partial liquidity to LPs. The transaction helped the fund bridge near-term capital needs and continue supporting its strongest assets in a slower exit market.

Direct Secondaries (Single or Multi-Asset)

Allows for targeted liquidity across one or more companies with speed, precision and alignment

Continuation vehicles, LP tenders, and structured solutions typically create liquidity at the fund or LP level without changing who manages the assets. While ownership may transfer to a new vehicle, the same VC remains the manager. Direct secondaries differ in that they involve selling shares in one or more companies to a new owner. In a full sale, the buyer assumes management of the position. In a partial sale, the GP typically remains involved alongside the new investor. This change in manager is what distinguishes direct secondaries from fund-level solutions and creates the opportunity to bring in a new partner who can contribute capital and strategic value.

Compared with fund-level solutions such as strip sales, direct secondaries offer greater flexibility in timing, counterparty choice, and structure. They are typically curated to meet objectives like returning capital, managing reserves, or simplifying operations.

A well-run process balances the GP’s objectives with buyer input, aligning on asset selection, pricing, and structure while managing communication across portfolio companies. Success depends on trust and relationships that enable smooth execution and sustain long-term alignment. Done right, these transactions deliver liquidity and optimize portfolio management.

While highly targeted, multi-asset transactions are not simple to execute. Asset selection takes time, internal alignment can be challenging, and management or co-investor consents can introduce execution risk. Transfer approvals and information sharing can further complicate timing and diligence. Pricing is more variable given company-specific dynamics, and selling even a portion of a GP-managed position means relinquishing a share of potential future upside. Direct secondaries work best when the GP has conviction, control, and a clear rationale for liquidity.

Practical considerations:

Which companies are best suited for a direct sale and why now?

How will upcoming financings or ownership changes affect execution?

Does the selected portfolio balance concentration, maturity and upside?

Are management teams aligned on timing and structure?

Will transfer rights or ROFRs impact execution?

Which counterparty is best aligned on price, structure and long-term partnership?

What ownership and board roles will be retained after closing?

Example:

After years of casual dialogue, an early-stage GP approached NewView with a desire to explore near-term liquidity options for several older funds in order to generate DPI and lock in substantial gains. Over the next five months, NewView and the GP curated a portfolio of 10 companies including both impact positions and tail assets, using position sizing and pricing (focused on intrinsic value) to create a compelling overall value proposition. The transaction prioritized direct share transfers and the GP retained approximately 70 to 90 percent of its original ownership in these companies, underscoring their conviction and ensuring alignment. After signing an exclusive LOI, the transaction closed. For the GP, the transaction delivered targeted liquidity while maintaining meaningful upside in the assets.

Solutions represent different tradeoffs for GPs

What to do next

Liquidity decisions define a GP’s discipline as much as investment decisions do. Whether you are addressing aging portfolios, reserve pressure, team transitions, or fund pacing, the most effective solutions are the ones built with careful intent.

Each structure comes with trade offs in timing, economics, complexity, and alignment. In practice, that means resisting reactive decisions. Rather than chasing available exits, GPs should return to first principles. What are you solving for? What alignment do you want to preserve? And how will this decision position your franchise for the next cycle?

At NewView Capital, we approach secondaries with a growth investor mindset. We look for opportunities to combine targeted liquidity with long-term value creation, and we believe GPs should have the flexibility to keep building. When managed with clarity and conviction, secondary transactions can strengthen both portfolio performance and GP-LP alignment. In today’s market, that discipline is what separates opportunistic selling from strategic liquidity.

Venture capital is in a liquidity gridlock. While the IPO market has begun to reopen and distributions have resumed, there is a significant backlog that can not—and we believe will not—be met via IPOs and M&As alone. Venture firms have built exceptional private value; there are roughly 63,000 U.S. venture-backed companies1 and over $4 trillion in global venture capital assets under management.2 Realizing that value at the right time, price, and structure is increasingly complex.

As GPs face growing pressure to deliver DPI, secondaries have become a core tool for portfolio management, with annual volume of direct secondaries projected to exceed $80 billion as of Q3 2025.1 Despite rising activity, venture secondaries remain a developing market. Most deals are bespoke, pricing can be opaque, and processes often vary by counterparty. That makes clarity of purpose even more important.

To identify the right secondary approach, GPs must start from first principles: what are they solving for? Is the goal to return a set dollar amount of DPI? To recycle capital within a specific fund? To manage orphaned assets after team changes? Or to take money off the table in high-performing companies? The priority can help dictate the best path.

At NewView Capital, we believe liquidity should be managed with the same discipline that drives great investing, with a focus on intrinsic value and long-term alignment across investors and companies. We developed this guide to help fellow GPs navigate secondaries with clarity, discipline, and conviction. While there is no one-size-fits-all playbook, understanding the leading options, and their benefits and trade offs, is the first step to choosing the right path for your firm.

Continuation Funds

Extends ownership in winners while providing LPs liquidity but are slow and complex to execute

Continuation funds allow GPs to move one or more portfolio companies into a new vehicle, offering existing LPs the choice to roll forward or sell.

Over the past year, the initial enthusiasm for continuation funds has been tempered by the realities of execution. Venture lacks the scale, valuation transparency and advisory infrastructure of private equity, making these transactions more difficult to close due to limited buyer depth, smaller deal sizes, and a higher bar for required returns. CVs work best for sought after, high-conviction assets that have a track record of growth that is expected to continue.

Continuation vehicles are among the most complex and time consuming to execute. They require coordination across LPs, portfolio companies, advisors, and new investors. Fair pricing requires third-party validation through valuations, LPAC approvals, and competitive bids from secondary buyers in a shallow venture market. These transactions often take several quarters and rely on clear communication and alignment to maintain confidence among stakeholders.

Non-RIA managers face additional structural hurdles. Firms relying on the venture capital adviser exemption are not permitted to hold more than 20% in non-qualifying assets at the fund level, which can make a traditional continuation fund infeasible. A ‘synthetic’ approach is possible but requires splitting the existing partnership into sub partnerships, amending the LPA, and obtaining LP consent, a costly and time-consuming process that carries regulatory risk if later deemed non-compliant.

For the right manager, CVs can elegantly extend ownership, deliver liquidity to LPs, and demonstrate conviction, but they demand significant preparation and alignment. These transactions are typically backed by large secondary funds and institutional LPs that can underwrite multi-asset portfolios within venture and growth equity.

Practical considerations:

Will regulatory or fund constraints (e.g. the 80 percent test) affect feasibility?

Are LPs aligned on the rationale and overall structure?

Is the GP team eligible for a carry reset or other incremental economics?

Is the portfolio composition compelling and supported by clear selection criteria?

Has an independent fairness opinion and valuation been completed to validate pricing?

Example:

A large multi-stage manager pursued a continuation vehicle to extend ownership across a curated portfolio of ten late-stage companies with strong growth potential. The initial proposal drew pushback from LPs who felt the mix included too many mid-performing assets and not enough of the manager’s top-tier holdings. In response, the GP re-curated the portfolio to include a greater concentration of high-quality companies, engaged an independent valuation advisor, and invited multiple secondary buyers to provide competitive bids. To maintain alignment, the firm shared detailed company-level data, held several LPAC sessions to review structure and economics, and clarified how carried interest would be allocated between vehicles. The revised transaction gained broad support, delivering liquidity to selling LPs while allowing the GP to retain and continue supporting its most valuable assets. The process took roughly nine months from initiation to close.

Strip Sales

Creates partial liquidity across a portfolio while preserving fund control

Strip sales allow GPs to sell a partial, non-controlling interest across a portfolio, typically 20 to 30 percent of each company, to a secondary buyer. These transactions provide liquidity without changing fund terms and can unlock value mid-fund without disrupting governance.

They are especially useful for GPs managing broad portfolios where multiple companies still have meaningful upside. Strip sales can return capital to LPs, reinforce DPI ahead of a fundraise, relieve pressure on follow-on reserves, and preserve control. These transactions generally attract secondary funds and institutional LPs seeking diversified venture exposure.

Because they involve many assets, strip sales are often complex. Negotiating across a full portfolio requires close coordination between the GP, secondary buyer, and portfolio companies to align on scope, valuation, and transfer mechanics. Pricing can also be more challenging as buyers don’t have discretion and must underwrite a cross-section of assets. This can result in higher discounts than for direct multi-asset or single-asset sales.

Practical considerations:

How will the portfolio be priced? Asset by asset or on a blended basis?

Will LPs support the rationale and treatment of proceeds?

How will buyer diligence across multiple companies affect the timeline and execution?

Does the structure retain sufficient exposure to high-conviction assets?

Will pricing dynamics impact the holding value of remaining ownership?

Example:

A GP managing a 2015 fund with 30 active companies and a new fundraise approaching needed to demonstrate DPI without giving up control of its best assets. The firm pursued a 25 percent strip sale across the portfolio, providing partial liquidity to LPs and freeing up reserves for follow-on investments. To coordinate the sale, the GP needed to obtain transfer consent from each company and update valuations to reflect uneven performance across sectors. The GP organized and managed the process directly, preparing data room materials, aligning company management teams on disclosure, and engaging with multiple buyers to benchmark pricing. Negotiations focused on achieving fair blended valuation while preserving future upside participation. The transaction returned capital to LPs and preserved governance rights while giving the buyer diversified exposure across the fund’s entire portfolio.

LP Tender Offers

Offers optional liquidity to LPs without altering fund structure

LP tender offers allow GPs to offer liquidity to existing LPs at a negotiated price usually facilitated by a secondary buyer. LPs can choose whether to participate, while the fund’s structure and underlying assets remain unchanged.

This structure is most useful when some LPs are seeking liquidity and others prefer to hold. It allows the GP to meet divergent investor needs without restructuring the fund or selling specific assets. It can also be a useful way to clean up the LP base or offer flexibility without altering fund construction.

While operationally straightforward, LP tenders offer less control than other secondary structures. The GP cannot select which LPs will participate as sellers and limited uptake may reduce the usefulness of the process. Pricing is typically driven by market appetite rather than intrinsic asset value and timing depends on LP responsiveness. These transactions are typically led by secondary funds, sometimes alongside institutional LPs or fund-of-funds, acquiring LP interests through GP-organized processes.

Practical considerations:

How will pricing be determined and communicated to LPs?

Will participation levels be sufficient to complete the transaction?

Are selling LPs’ motivations aligned with the fund’s long-term strategy?

Has the LPAC reviewed and approved the process?

Example:

A GP managing a 2018 fund heard from several LPs, mostly smaller family offices, that they were over-allocated and wanted liquidity. The larger institutional LPs preferred to hold. The GP needed a way to meet these divergent needs without restructuring the fund, so they arranged a tender offer for up to 20 percent of the fund backed by a single secondary buyer. The process required coordination across LPs with varying liquidity goals as well as clear communication to maintain alignment and trust. The GP worked with counsel to prepare detailed disclosures and positioned the transaction as part of proactive portfolio management ensuring participation was entirely optional and pricing reflected fair market value. The offer was fully subscribed, providing liquidity to selling LPs while preserving continuity for long-term investors and reinforcing confidence ahead of the next fundraise.

Preferred Equity and Structured Solutions

Delivers flexible capital for liquidity without selling ownership

Structured solutions such as preferred equity, profit sharing notes, and other hybrid instruments allow GPs to raise capital against a fund or asset without triggering a sale. These structures are typically used to provide interim liquidity, refinance obligations, or fund follow-ons when exits are slow or valuations are misaligned.

Preferred equity sits between debt and equity. Investors receive downside protection and a return with optional upside sharing tied to future cash flows, typically attracting secondary and credit-oriented investors offering flexible liquidity solutions. These deals can be negotiated at the fund or asset level and are especially useful when buyers and sellers aren’t aligned on valuation or timing.

For GPs with conviction in future value, structured solutions can create liquidity without giving up control, exposure, or board seats. They offer flexibility in tailoring terms to portfolio performance, reserve strategy, or LP dynamics.

While powerful, these deals are complex, often expensive, and LP sentiment about these structures is mixed to negative. Structuring repayment waterfalls takes time and legal support, and the cost of capital may be high relative to selling assets. Poorly designed structures can create misalignment, cash flow stress, or excessive dilution if exits take longer than expected. They are best suited for managers with predictable near-term liquidity events and a clear rationale for raising capital without selling.

Practical considerations:

What visibility is needed to underwrite repayment terms?

Will repayment be tied to specific exits or overall fund cash flows?

How will preferred returns flow through to existing LP distributions?

Are governance and incentives aligned between GP and capital provider?

Example:

A GP managing a 2016 fund with several late-stage winners and upcoming financings needed liquidity to support follow-ons while maintaining exposure to key assets. With limited reserves and few near-term exits, the GP structured a preferred equity solution at the fund level to unlock capital without changing ownership. The structure provided upfront liquidity in exchange for a capped share of future proceeds, allowing the GP to fund follow-ons and deliver partial liquidity to LPs. The transaction helped the fund bridge near-term capital needs and continue supporting its strongest assets in a slower exit market.

Direct Secondaries (Single or Multi-Asset)

Allows for targeted liquidity across one or more companies with speed, precision and alignment

Continuation vehicles, LP tenders, and structured solutions typically create liquidity at the fund or LP level without changing who manages the assets. While ownership may transfer to a new vehicle, the same VC remains the manager. Direct secondaries differ in that they involve selling shares in one or more companies to a new owner. In a full sale, the buyer assumes management of the position. In a partial sale, the GP typically remains involved alongside the new investor. This change in manager is what distinguishes direct secondaries from fund-level solutions and creates the opportunity to bring in a new partner who can contribute capital and strategic value.

Compared with fund-level solutions such as strip sales, direct secondaries offer greater flexibility in timing, counterparty choice, and structure. They are typically curated to meet objectives like returning capital, managing reserves, or simplifying operations.

A well-run process balances the GP’s objectives with buyer input, aligning on asset selection, pricing, and structure while managing communication across portfolio companies. Success depends on trust and relationships that enable smooth execution and sustain long-term alignment. Done right, these transactions deliver liquidity and optimize portfolio management.

While highly targeted, multi-asset transactions are not simple to execute. Asset selection takes time, internal alignment can be challenging, and management or co-investor consents can introduce execution risk. Transfer approvals and information sharing can further complicate timing and diligence. Pricing is more variable given company-specific dynamics, and selling even a portion of a GP-managed position means relinquishing a share of potential future upside. Direct secondaries work best when the GP has conviction, control, and a clear rationale for liquidity.

Practical considerations:

Which companies are best suited for a direct sale and why now?

How will upcoming financings or ownership changes affect execution?

Does the selected portfolio balance concentration, maturity and upside?

Are management teams aligned on timing and structure?

Will transfer rights or ROFRs impact execution?

Which counterparty is best aligned on price, structure and long-term partnership?

What ownership and board roles will be retained after closing?

Example:

After years of casual dialogue, an early-stage GP approached NewView with a desire to explore near-term liquidity options for several older funds in order to generate DPI and lock in substantial gains. Over the next five months, NewView and the GP curated a portfolio of 10 companies including both impact positions and tail assets, using position sizing and pricing (focused on intrinsic value) to create a compelling overall value proposition. The transaction prioritized direct share transfers and the GP retained approximately 70 to 90 percent of its original ownership in these companies, underscoring their conviction and ensuring alignment. After signing an exclusive LOI, the transaction closed. For the GP, the transaction delivered targeted liquidity while maintaining meaningful upside in the assets.

Solutions represent different tradeoffs for GPs

What to do next

Liquidity decisions define a GP’s discipline as much as investment decisions do. Whether you are addressing aging portfolios, reserve pressure, team transitions, or fund pacing, the most effective solutions are the ones built with careful intent.

Each structure comes with trade offs in timing, economics, complexity, and alignment. In practice, that means resisting reactive decisions. Rather than chasing available exits, GPs should return to first principles. What are you solving for? What alignment do you want to preserve? And how will this decision position your franchise for the next cycle?

At NewView Capital, we approach secondaries with a growth investor mindset. We look for opportunities to combine targeted liquidity with long-term value creation, and we believe GPs should have the flexibility to keep building. When managed with clarity and conviction, secondary transactions can strengthen both portfolio performance and GP-LP alignment. In today’s market, that discipline is what separates opportunistic selling from strategic liquidity.

This post is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation to invest in any securities. NewView may have an ownership interest in the company discussed, which may present conflicts of interest. The information presented is based on publicly available data (unless otherwise noted), and the company’s own statements, and NewView makes no representations or warranties as to its accuracy or completeness. This post is intended for financially sophisticated investors; NewView does not solicit or make its services generally available to the public. See Terms of Use for more information. Past performance is not indicative of future results. Any forward-looking statements are based on current expectations and involve risks and uncertainties; actual results may differ materially.